We want all our clients – current, past, and future – to be aware of our planning and expectations as we have begun what we expect could be a lasting turbulent time as fall out from Corona Virus concerns. This is not a “sky is falling” expression for our business or personal outlooks, however, we feel it’s important to be aware and have a plan.

I will not pretend to have accurate facts or present opinions on Corona Virus or Covid-19. I will however share my outlook and opinion on the economic concerns that have begun, and I believe we will see lasting effects, in particular how I believe it pertains to Residential Real Estate.

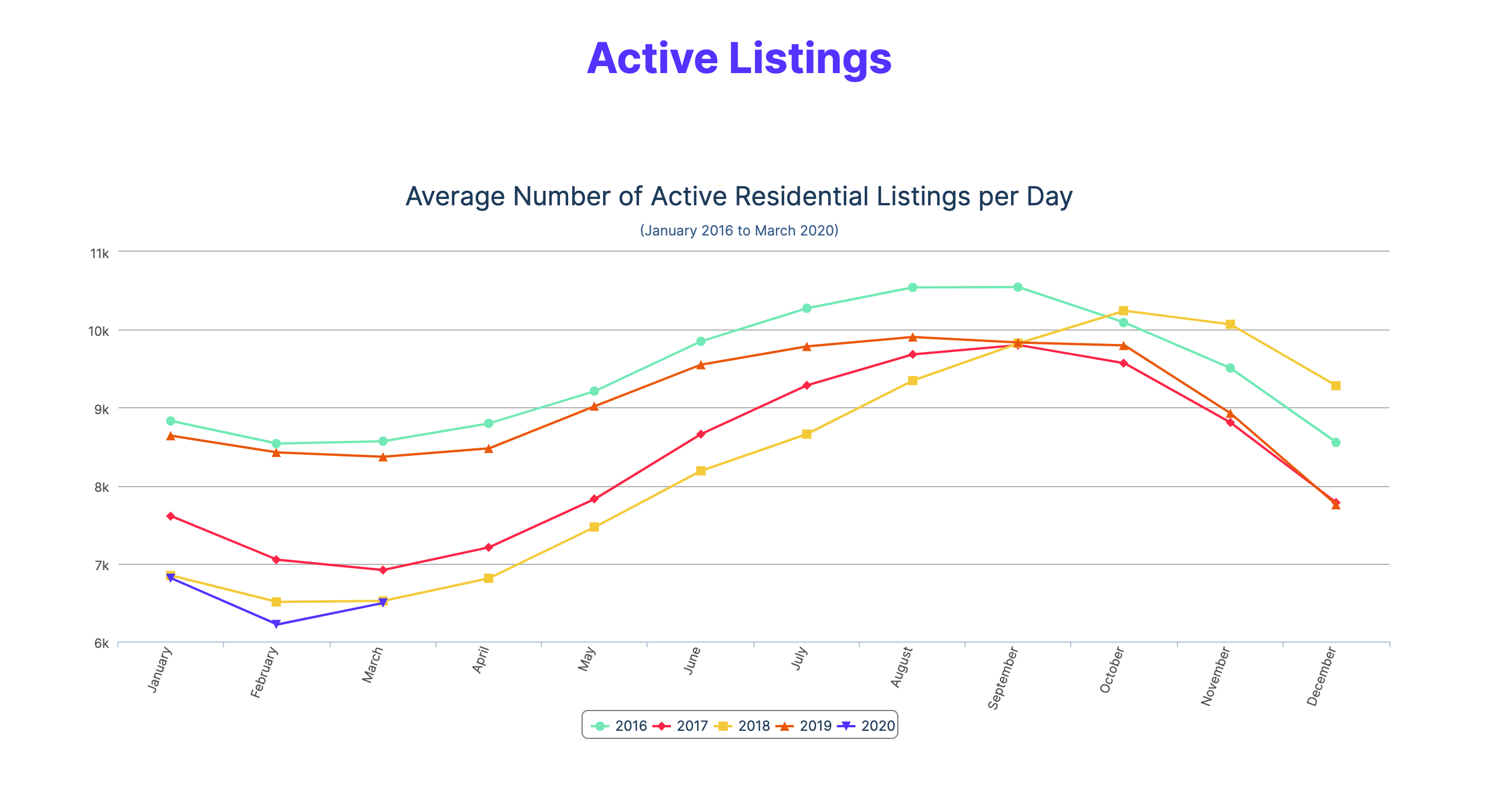

For some background, my father practiced real estate as a broker, investor, appraiser, and manager starting in the 70’s and through my growing up years, and I learned a lot. I have been licensed in Real Estate in Utah, and extremely active across many sectors since 2003. I am a large investor in residential real estate, our company manages many millions of dollars’ worth of real estate for clients, and our companies participate in hundreds of rental and sales transactions per year. This business is mostly all in Utah, however minimally in other western states, and I have spent time with clients in over 30 states over the years analyzing and consulting on real estate investing. That is to say, I have seen the market though a few ups, and a few downs, and many angles in between. Most notably of course the downturn which began in the 3rd quarter of 2008 when median home prices declined year over year until 2011. The only other time that has happened since statistics can be reliably tracked was 1 year in the 80’s. To be very clear, I don’t expect we are on the brink of a slide like 2008-2011.

Here are my two biggest takeaways having gone through that firsthand and having taken it on the chops in some aspects. 1st – those who were in a sound financial situation as it pertained to their real estate going in – came out even better. 2nd – Rents never saw a year over year decrease even though values saw four straight years of median price decreases. My personal rental portfolio saw increases throughout that four-year economic slide, in addition to the other tax and financial benefits of real estate ownership.

Tanking interest rates have already, and I suspect will continue to prop up the sales market – which in my opinion could have used some cooling – but certainly not a drop. That is great news for sellers, loan officers and brokers, and even buyers who plan to use lots of leverage - they can now afford a much bigger mortgage for the same monthly payment. I expect this will lead to temporary decrease year over year in inventory, jump in prices, and added frustration in a market that is already heavily multiple offer scenarios. I’ve lost multiple deals to multiple offer situations in the last few weeks, where my clients offered my recommended max market value, and others were willing to pay more. If the quarantine recommendations or mandates rapidly increase, and we are all on lock-down, of course that will alter that outlook. One difference now vs. 2008-2011 is that avg. mortgage rates at the end of 2008 were 5.1%, that’s after the slide had been going for over a quarter, and banks and lenders were closing doors and being shut down left and right. Current rates at just the beginning of this current storm are already hovering at 3%, lower than where they bottomed out in 2013 after that recovery was already gaining steam. For perspective to the 80’s where we only saw one year of median price declines, peak rates hit 18.6%, and they had a floor at 9.1%. I don’t have an opinion on good or bad policy, or other contributing factors here, but those are some facts that will sustain prices in my view. (source: https://fred.stlouisfed.org/graph/?g=NUh)

Cancelled conventions, summits, and other large gatherings, as well as closing of tourist attractions around the country and the world have already lead to a massive financial loss in the travel, entertainment, and hospitality industries – if you want proof, log into your favorite travel search engine and compare your dream vacation now v. the last time you checked, if you can even get there. To what extent it spills over to other industries directly is not yet known, but it will. This will have a lasting economic effect, which of course will also affect Real Estate.

Trickle down consequences I expect to see soon are: an increase in late and non-paid rents for landlords from tenants and missed mortgage payments eventually leading to more foreclosures among homeowners. Landlords will have to make some plans and decisions of how they want to handle late or missed rent payments. And for over-leveraged paycheck to paycheck owners, it will take some time, but there will be an uptick of foreclosures. To give you some relevance on foreclosures; Salt Lake County has seen approx. 4-5 avg. foreclosure filings per day over the last couple years, in 2011 there were approx. 25 per day. Borrowing criteria has been much higher for the last 10 years, so I don’t expect we’ll see foreclosure rates like we did prior.

I’ll tell my management client owner’s what my plan and policy will be on my own rentals, which is a change from our standard company policy to date. Our owner clients will need to determine their stance and let us know if they would like to adopt any changes.

- Current company policies:

- We do not waive late fees

- If someone is late and they:

- (a) don’t reach out to us to make a payment arrangement, we serve a 3-day pay or vacate notice within 3 business days of the 5th. If that notice expires, and there still has been no communication, we submit it to our attorney for eviction which takes approx. 3 weeks.

- (b) respond and/or reach out to us, we will create a payment plan with them, if we deem it to be in the best interest of the property owner, and the tenant shows ability to perform. Still serve them a notice to pay or vacate, so that if they fail to perform on the agreement, we aren’t waiting another 3 days to file.

- No payment arrangement can carry a balance over current months end.

- My personal changes for tenants effective immediately (it should be noted these temporary changes will not be shared directly with tenants):

- Late fees may be waived if tenant provides logical and documented reason for being late directly related to changes in their income or health status, or that of other breadwinners in the property based on current economic factors

- Payments plans may extend beyond the end of the month, with agreement from the property owner

- Evictions will be turned over to the attorney only after a tenant is a full month late AS LONG AS THEY HAVE COMMUNICATED WITH US, and we can determine they are trying to get funds.

- Balances will not be allowed past due of 45+ days without being turned over to eviction

In summary, I don’t propose that I know what the next 6 weeks, 6 months or 6 years will look like. What I do know is that our company is prepared to weather a storm, and we have weathered past storms. Our clients are in good hands, with experience on their side. Throughout history, it is evident that with each economic cycle there can be massive increases in wealth both in good times and bad, it depends on one’s positioning, mental state, and adaptivity. If you would like to discuss in more detail your specific situation as it pertains to your real estate needs, I’m happy to schedule a time and discuss thoughts and ideas.

Best,

Regan Richmond

Utah Select Realty – Associate Broker

True Options Real Estate & Richmond Consulting